Understanding Your Credit Score and Reports

This article explains the importance of understanding and accessing credit scores and reports. It covers how to obtain FICO scores through various lenders, how to regularly check credit reports, and the legal rights for free reports. Tips are included for managing credit effectively, ensuring accurate information, and using reliable sources. Whether you're applying for a loan or monitoring your credit health, knowing these steps helps you stay informed and make better financial decisions.

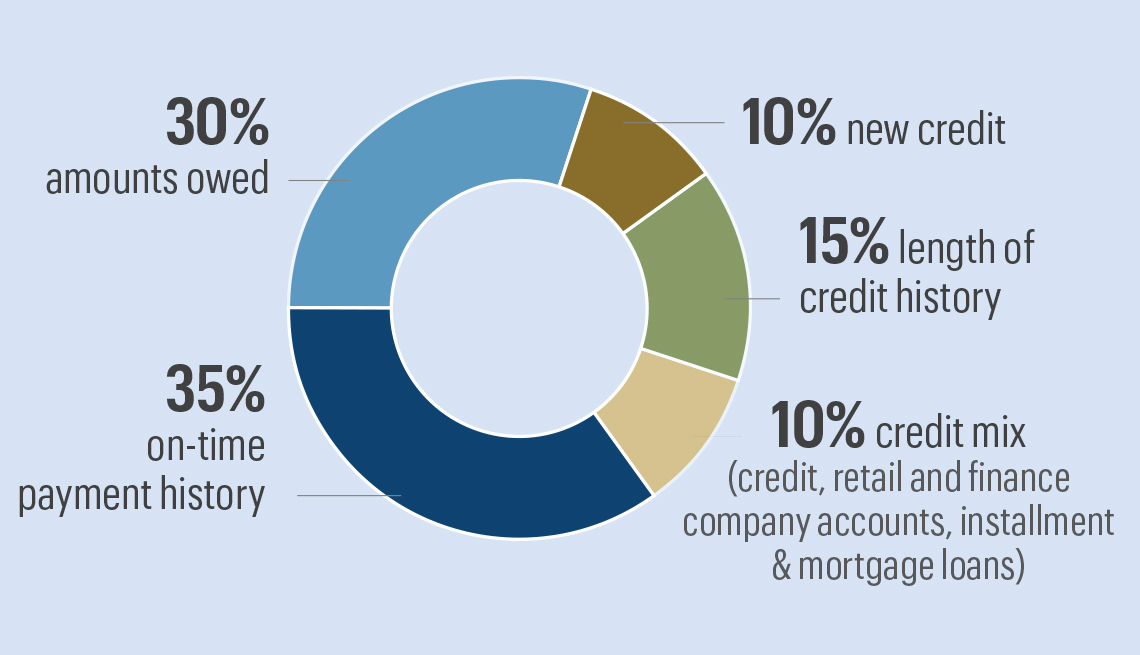

Understanding Your Credit Score is essential for managing your financial health. Knowing how to access your credit report and FICO score helps you monitor your financial standing effectively.

How can I obtain my credit score?

A: The most reliable credit scores are FICO scores.

Banks like Discover and Barclay offer FICO scores based on TransUnion reports.

Citi provides an Equifax-based FICO score.

American Express and Chase Slate display Experian FICO scores.

You can check your credit score through online banking or mobile apps of these credit card providers. Keep in mind that different models of FICO scores are used by various institutions, so scores may vary depending on who pulls them. Additionally, third-party websites may offer alternative scoring models, but these are not official and can differ significantly from FICO scores. Such sites often let you view your credit report along with your score.

How can I get my credit report?

A: Regular review of your credit report is recommended, especially if you notice discrepancies or a drop in your score. It's advisable to seek your report proactively, even if your score remains stable.

Under the Fair Credit Reporting Act (FCRA), you are entitled to one free credit report annually from each of the three major bureaus via www.annualcreditreport.com. A good practice is to request a report from one bureau every four months to keep track of your credit history consistently.

You can also request free reports after applying for credit products like credit cards, loans, or insurance, especially if your application is denied or results in adverse actions within 60 days. These reports can be obtained from Equifax, TransUnion, and Experian.

Once you have obtained your Experian report, you can view it repeatedly on their website using your report number.

Third-party platforms like Credit Karma, Credit Sesame, Mint, Credit.com, Quizzle, and Credit Card Score also provide free access to credit reports from different bureaus.

Note: Individuals who have recently obtained an SSN might face verification hurdles and may need to provide additional documents to access their credit reports online.