Nike's Rapid Growth Signals Continued Market Potential

Nike showcases strong growth driven by record revenues, digital expansion, and recovering demand, positioning itself for sustained long-term success. Experts remain optimistic, citing the company's innovative strategies and robust market presence as key factors for future stock appreciation. Nike’s focus on digital sales and consistent dividend increases make it a compelling investment choice amid market fluctuations.

Recently, Nike (NYSE:NKE), a leading name in sportswear, has experienced a remarkable surge in stock value.

This upward momentum suggests Nike is adopting a new financial approach that supports sustainable long-term growth. Driven by robust sales figures, the company's share price has increased by roughly 25% recently.

At the core of this growth are record-breaking quarterly revenues—over $12 billion for the first time in the company's 50-year history. This sales achievement, post-pandemic, signals a new phase of rapid expansion, making Nike’s stock highly appealing to investors.

However, after such a boost, questions arise: How long will this growth last? Is the stock overvalued? To answer these, we need to examine the current challenges Nike faces.

Factor 1: Recovery of pent-up demand

During the pandemic, restrictions and event cancellations hampered Nike’s sales. In the quarter ending May 2020, sales dropped approximately 40% from the pre-pandemic USD 10 billion.

As the U.S. economy reopened this spring, Nike’s sales rebounded strongly, fueled by accumulated demand. By May 31, global sales nearly doubled, with direct-to-consumer shipments soaring over 70%.

In China, Nike also performed well, with sales increasing 17% last quarter to $1.9 billion, despite political sensitivities.

Looking ahead, Nike forecasts double-digit sales growth for the current fiscal year ending next May. Management expects faster growth in the first half, reflecting strong consumer interest. CEO John Donahoe emphasized Nike's competitive edge and deep consumer connections.

Factor 2: Digital transformation driving growth

The pandemic accelerated Nike’s shift to online retail, establishing a direct-to-consumer model that boosts efficiency and margins. Over recent quarters, digital sales jumped by over 80%, surpassing revenue targets and representing 30% of sales in China.

This success isn't luck. CEO John Donahoe, formerly of eBay, took over in January 2020 and prioritized digital channels, including Nike’s website and app improvements, and cutting wholesale partners like Amazon.

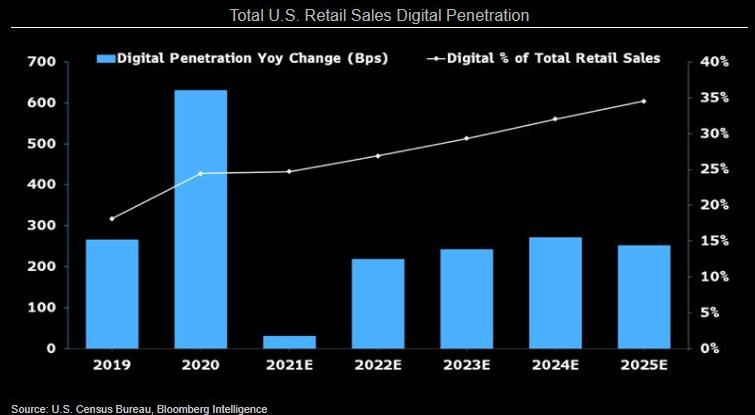

The pandemic hastened e-commerce adoption, transforming U.S. retail. Nike projects online shopping will grow from 14% to 35% of total retail sales by 2025, with China’s online sales expected to rise to 60% of total sales.

Factor 3: Positive analyst outlook

Supported by these trends, Wall Street remains bullish. With a shift to more profitable online sales, profit margins are increasing, encouraging analysts. Among 34 surveyed, 29 rate Nike as an outperform, with forecasts of an 8% stock rise in the coming year.

Oppenheimer recently raised Nike’s target price from $150 to $195, citing underestimated business potential. Randal Konik at Jefferies praised Nike’s global consumer base and tech-driven brand loyalty, assigning a "Strong Buy" rating.

Nike expects over 10% revenue growth in the upcoming fiscal year, exceeding $50 billion, driven by direct-to-consumer sales, which contributed 19% last year.

Factor 4: Attractive dividend prospects

While current dividend yields are modest at 1%, Nike’s consistent dividend increases—annual hikes for 19 consecutive years—enhance its appeal to long-term investors. The payout ratio hovers near 30%, indicating room for future dividend growth even during economic downturns.