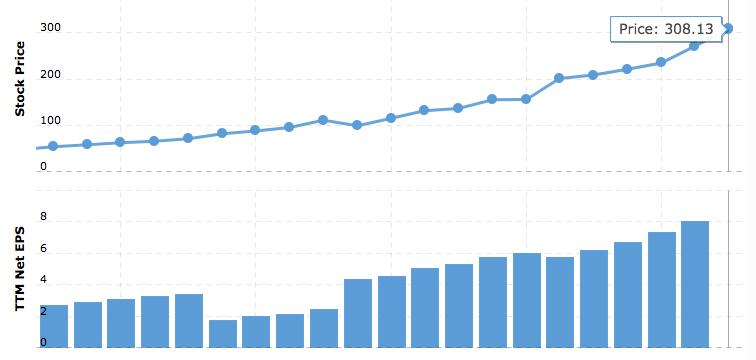

Microsoft's Latest Financial Results Signal Robust Growth in Cloud and Software Sectors

Microsoft continues to demonstrate impressive financial health with strong growth driven by cloud and enterprise solutions. Its strategic investments in Azure, acquisitions, and new product launches bolster its market position, making it a leading choice for investors seeking long-term durability in technology stocks. Despite high valuation, ongoing expansion and innovation promise sustained performance, reinforcing Microsoft's role as a dominant force in the digital economy.

The current earnings season presents a challenging landscape for investors, with noticeable disparities among leading tech giants. Unlike previous quarters, the financial reports reveal a divergence—some outperforming expectations, others falling short. Facebook’s recent report missed the mark except during early pandemic-affected periods, while Snap’s lowered revenue forecasts have dampened market confidence in ad revenues. Conversely, Google’s report showed strong revenue and profit growth, although growth momentum has slowed. Amidst inflation and supply chain pressures, Tesla’s impressive results buoyed market sentiment, and yesterday’s post-market release from Microsoft continues to reinforce a bullish outlook for the Nasdaq.

Microsoft announced a stellar earnings report, with revenue and profit both surpassing forecasts. The company reported $45.3 billion in revenue, up 22% year-over-year, exceeding analyst expectations of $43.93 billion. Earnings per share reached $2.71, well above the expected $2.07, while net profit soared 48% to $20.5 billion. The breakdown showed product revenues (including systems and office software) at $16.6 billion, up 5.2%, and service revenue (cloud computing and related services) at $28.7 billion, increasing 34%. Gross margins remained stable, with product gross profit at 77.2% and service margin at 65.7%.

Microsoft’s growth is primarily driven by its service divisions, notably cloud computing—akin to Amazon’s AWS. While profit margins are thinner than traditional products, the long-term growth potential remains significant, as the data-driven economy propels digital transformation projects worldwide. Microsoft's Azure is a key competitor to Amazon AWS, benefiting from integration with Office 365 and other enterprise software, securing its market position. An industry report highlighted Azure’s competitive share in the global cloud market, with Microsoft planning to expand its data center footprint by building 50–100 new facilities annually—signaling sustained double-digit growth prospects for cloud services.

Office 365 also showed strong performance, with 23% growth, indicating a steadfast ecosystem expansion. Additionally, advertising sectors such as search and news saw a 40% annual increase, underscoring the company’s diversified revenue streams. On the cost front, research and development expenses totaled $5.6 billion, representing 12.4% of revenue—down slightly from last year’s 13.25%—yet rising in absolute terms. Marketing costs stood at $4.5 billion, or 10% of revenue, decreasing from 11.4%, which points to improved efficiency. Administrative expenses were low, at $1.29 billion, constituting only 2.8% of revenue, helping sustain an impressive operating profit margin of 44.7%.

Microsoft’s ecosystem boasts high barriers to entry and strong growth prospects, especially in cloud services anchored by Azure. The company has also launched new hardware—including Surface PCs—and acquired security startups CloudKnox and RiskIQ. Notably, hiring Amazon veterans like Charlie Bell for cybersecurity signals increased focus on data security amidst recent high-profile incidents. Despite current valuations around 38 times earnings, its robust revenue growth in cloud computing and steady performance across divisions justify the premium. In the medium to long term, Microsoft remains an attractive investment opportunity for those seeking resilient growth in the technology sector.